|

Monday, May 18, 2009

SEED has a set of short video responses to the question "Are we beyond the Two Cultures?", a reference to the split between the arts & humanities types and the science types. Steven Pinker discusses several ways in which the arts can benefit from working with the sciences, such as gaining a better understanding of human attention, visual processing, and so on. In his book The Blank Slate, Pinker argues that one reason that 20th C. art and architecture have been such huge flops is Modernism's denial of a basic human nature, both in terms of how the mind works and what things push our pleasure buttons. But aside from what has been going on in academia and the art gallery world, where does the art-consuming public stand on bridging the Two Cultures?

If we are to believe Tom Wolfe's account in From Bauhaus to Our House, in the first several decades after WWII, most of the elite considered it cool to sit in (or at least display) furniture that embodied the Modernist aesthetic. He emphasizes that Mies van der Rohe's Barcelona chair was particularly sought after. So, some decades later, how much does the public value Modernist design as compared to design whose forms are derived more from nature? (The latter forms appeal to what E.O. Wilson calls "biophilia," or our native apprecation for natural forms. This idea goes back at least to the mid-19th C., when the British architect Owen Jones wrote The Grammar of Ornament, available online in full and in color. It sought to bridge the gap between the arts and the sciences by investigating the general laws of aesthetics in ornamentation, and especially by pointing to the central role that nature-based forms play.) Searching Amazon.com's home & garden section for Modernist keywords "Barcelona chair" gives 957 results (other searches for this item give fewer hits), "Mies" gives 435, "Corbusier" gives 284, and "Eames" (who is much more palatable) gives 1,258. Contrast this with Art Nouveau keywords: "Tiffany lamp" alone gives 10,381, while the broader "Tiffany -breakfast" (to remove Breakfast at Tiffany's memerobilia) gives 16,565 hits. Price differences don't seem to account for this, since the objects from both styles are moderately expensive. The same order-of-magnitude difference shows up for searches of Ebay.com's home & garden section too. "Tiffany lamp" gives 2,003 results, while "Barcelona chair" and "Mies" each give about 40, "Corbusier" gives 303, and the less-insane "Eames" gives 466. Finally, searching AllPosters.com gives 147 hits for "Tiffany" (Studios) and 191 for "Gaudi," compared to only 22 for "Eames," 38 for "Corbusier," and 16 for "Mies." So, as far as the art-buying public is concerned, most people seem to belong to the Third Culture already. It's only arts academics, critics, and others in the business of art who insist on a sharp divide between the arts & humanities and the sciences. After all, they have their territory to defend from the ever-encroaching sciences, whereas outsiders are disinterested. I found something similar when I looked at the under- and over-valuations of composers and of painters as well: most of the art-buying public values mid-late 19th C. music and painting, mostly ignoring the Modernists. When the elite art world abandoned its interest in the sciences, more or less as a fashion statement, it doomed itself to silliness and obscurity. Science types already read a lot outside of their main area, so we don't have terribly far left to go. However, arts & humanities types flaunt their ignorance of the sciences -- unlike Alberti or Owen Jones -- so that the burden of "closing the gap" falls more on them. Labels: arts, culture, science

Sunday, April 19, 2009

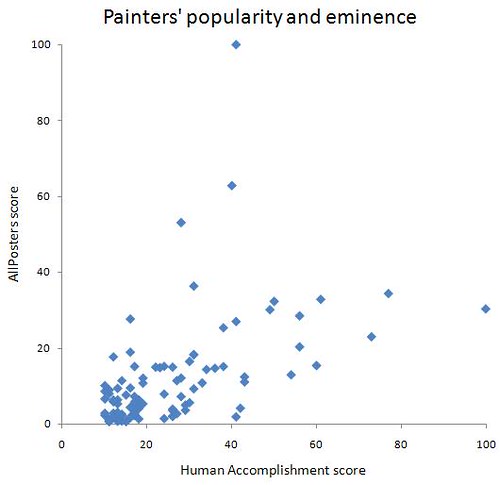

As a follow-up to the previous post on measuring the price-to-earnings ratio of composers, I've done the same thing for painters. The motivation is the same, and I'm still using the painter's score in Charles Murray's Human Accomplishment to measure earnings (the more objective valuation). Here, instead of measuring price (the more fashion-driven valuation) with the number of works available at Amazon.com, I'm using the number of works available at AllPosters.com, the main place that people visit to buy inexpensive high art.

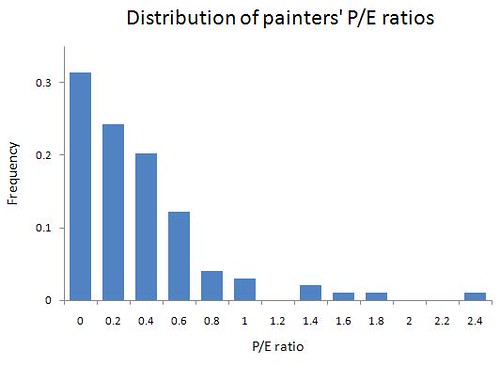

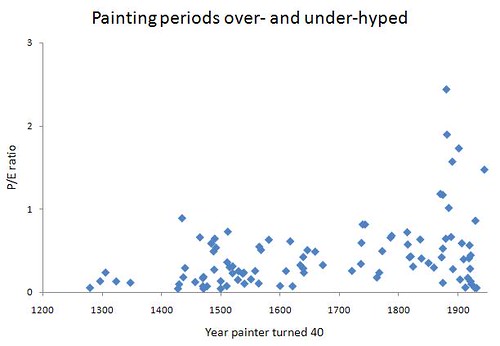

The AllPosters score is simply number of works available, divided by the max for any artist (which happens to be for Monet), multiplied by 100. So, like the HA score, it is a measure of how valued an artist's works are, using the most highly valued artist of all as a reference point. A look at the data shows several similarities to the case of composers, suggesting that -- for example -- we overhype a certain time period in general, even though it could arguably be the peak for one art form and yet be only mediocre for another art form. We are more likely to fall for the whole zeitgeist, rather than ruthlessly discriminate and have a separate "favorite period" for different art forms. Anyway, let's get to the results. I've uploaded the dataset here, where you can copy & paste the text into an Excel spreadsheet to play around with it yourself. I'm only using painters because the sculptors and architects don't have much available at AllPosters -- people want to buy prints of paintings, not of sculptures. Although I haven't used them in the analysis, I've still included the sculptors and architects in the raw data. This only excludes 12 of 111 artists, and they're pretty spread out across time periods. As with composers, the agreement between encyclopedia writers and educated laymen is pretty close. Spearman's rank correlation between the HA score and the AllPosters score is rho = +0.58 (p less than 10^-6). As before, a fair amount (about 34%) of the variation in subjective valuations can be accounted for by variation in fundamental worth, but that still leaves plenty of room for hype to influence poster-buyers. Here is a plot of the two scores:  The two biggest outliers are Monet, who dominates the poster market but is considered second-tier in encyclopedias, and Michelangelo, who dominates encyclopedias but doesn't appear on many people's walls. This could be due to a lot of his work being sculpture and architecture. (None of the results are affected by counting Michelangelo as a sculptor / architect and removing his data-point from the analysis.) Picasso also gets a lot of coverage in encylopedias, while not attracting much attention from poster-buyers. As with Schoenberg among composers, this may suggest that Murray's decision to use 1950 as a cut-off was still a bit too late to fully remove the effects of hype. Still does a very good job, given that only a couple of probably over-rated Moderns have P/E ratios that say they're actually under-rated (e.g., Picasso, Max Ernst, de Chirico). The clearest case of a painter who is very eminent is encyclopedias but fairly neglected by the lay public is Raphael -- his HA score is 73, while his AllPosters score is 23. Most people my age wouldn't even recognize him, were it not for the Teenage Mutant Ninja Turtle named after him. For fun, here are the top 10 under-valued and over-valued painters, where hype increases as you go down either list: Top 10 under-valued painters Masaccio Pol de Limbourg Antonio del Pollaiolo Max Ernst Giorgio de Chirico Cimabue Piet Mondrian Hugo van der Goes Martin Schongauer Frans Hals Top 10 over-valued painters Marc Chagall Fra Angelico Henri Rousseau Edgar Degas Camille Pissarro Salvador Dali Vincent Van Gogh Henri de Toulouse-Lautrec Pierre-Auguste Renoir Claude Monet And as we saw with composers, the P/E ratios of painters are highly skewed, with most painters being under-rated and a tiny handful who are blown out of proportion. As before, a log-normal (or maybe exponential) distribution probably underlies the pattern. Here is the distribution, where the average is 0.4:  Finally, here is a look at how P/E ratios vary based on when the painter flourished:  Just as with composers, those painters who flourished in the second half of the 19th C are the most over-valued. In a response to my composers post, Steve Sailer suggested that the time series showed that Western music reached its pinnacle during the Late Romantic period, perhaps because it was more profound than what he considers the daintier Classical-era music. But the painters who are responsible for inflating the hype of late-19th-C painting cannot be said to represent the perfection of technique, the profound rather than the light, and so on. These are the Impressionists and some Post-Impressionists, after all -- not their Academic contemporaries like Bouguereau. The only commonality with their musical contemporaries is a preference for expression, emotion, and well, the impressionistic. So, there are two explanations for the over-valuation of late-19th-C music and painting: 1) there is currently an irrational fashion bubble for that time period -- it had to be some period, so why not that one? The bubble would encompass the entire zeitgeist, regardless of whether the different parts of it represented the pinnacle of art in their respective media. Or 2) the art-consuming public is more sentimental than judges of art, so that the public tends to over-value time periods that gave greater emphasis to the emotions per se, independent of their artistic merit or the profundity of emotion expressed. This second explanation includes all class-based explanations, such as the one that says that academics favor aristocratic art, while the lay public is mostly upper-middle class professionals who have a weak spot for the high point of art consumed by the bourgeoisie. It was the new merchant class, remember, that was responsible for cleaning up the lurid spots left by the aristocratic and lower classes -- ending public hangings (and then hangings altogether), campaigning for animal rights, looking upon duels and other fights as barbaric rather than civilized, and so on. So we could just be seeing a class phenomenon, given that the middle class is more sentimental. Labels: arts, culture, Economics

Tuesday, April 07, 2009

The concept of price-to-earnings ratio can be extended to anything that has an objective, fundamental value and a subjective value that people give to the thing -- assuming these can be measured, however crudely. The ratio gets bigger when the price goes up while the thing is still generating the same amount of earnings, or when it generates less earnings while being priced the same. So, larger values of this ratio mean that the thing is overhyped, while smaller values mean it's overlooked.

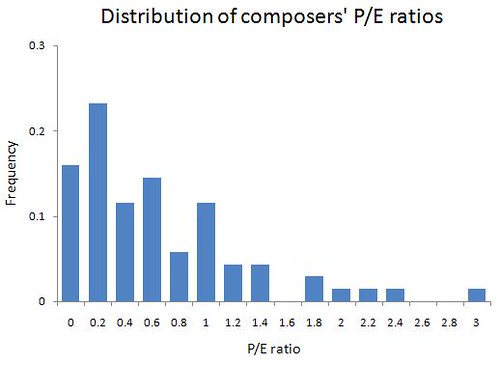

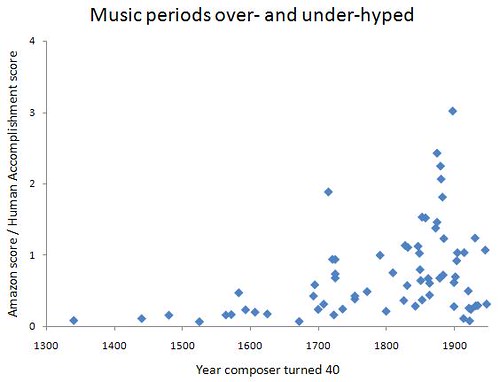

When lots of instances of the same thing are over-hyped, and when this over-hyping steadily increases for a stretch of time, we have a bubble. When people wake up to reality and the P/E ratio plummets, the bubble bursts. See the first graph in the Wikipedia link above for stock market data that show this relationship. These bubbles are counter-examples to the efficient-market hypothesis, which holds that prices already contain all known information about the stock -- or, say, the house. Under the hypothesis, a smarty-pants could not predictably outperform the stock (or housing) market, since they can't know anything that everyone else does not already know. But in reality, people who didn't believe the hype about houses, such as hedge fund manager Steve Eisman, got rich by betting that everyone else was nuts. Below the fold, I develop a rough P/E ratio for Western composers, calculate it for 69 eminent ones, and discuss some applications. For the measurement of the composer's fundamental value, I use his score in Charles Murray's Human Accomplishment, which measures how much space he is given across a wide variety of music encyclopedias -- how deserving he is. It's true that article writers could be in the midst of an irrational bubble for Beethoven and devote more space to him than he merits, but by using encyclopedias across many different languages and time periods, Murray protected as much as possible against this bias. He also excluded figures who flourished in the second half of the 20th C, just in case article writers were still affected by a recent bubble. For the measurement of the public's subjective valuation of the composer, I use the number of results returned from a search of his name in the "classical" section of Amazon's music section. (This is the name listed under "composer" in the work's webpage.) Unlike the number of Google results, the number of works offered for sale is a good measure of how much hype the composer enjoys among real consumers of classical music. I normalize these results by dividing by the maximum number of results (which happens to be for Mozart) and multiplying by 100, to put it on a 0 - 100 scale, as with the HA scores. The measurement of how under- or over-valued a composer is, the P/E ratio, is just the scaled Amazon score divided by the HA score. Higher P/E scores suggest he is over-hyped -- if two composers have the same amount of space devoted to them by those in the best position to objective judge the composers' excellence, the one with many more works being offered enjoys the influence of hype. And so does the composer who has the same number of works being offered as another, but who has much less space devoted to him in encyclopedias. One drawback here is that, unlike the P/E ratio for stocks or houses, the two parts of the ratio aren't measured in the same units, or even close -- they are a scaled measure of column inches and a scaled measure of works being offered. So the ratio here doesn't have an intuitive interpretation. But if we just want to see who's over- and under-valued, that doesn't matter. I calculated this P/E ratio for anyone in Murray's list of Western composers who scored 10 or above on his 0 to 100 scale, which yielded 69 data-points. To see all composers' data, you can download the spreadsheet here by clicking on view data and copying & pasting (as text) into an Excel file. Briefly, though, for fun here are the 10 most under- and over-valued composers, where the P/E ratio increases as you go down each list. (Thus, Willaert suffers the least from hype, and Puccini the most.) Bear in mind that "over-valued" does not mean "junk," and "under-valued" does not mean "awesome" -- only that the composer is given too much attention, or too little. 10 most under-valued composers Adrian Willaert Jean-Baptiste Lully Anton Webern Guillaume de Machaut Guillaume Dufay Arnold Schoenberg Josquin des Prez Giovanni Pierluigi da Palestrina Jean-Philippe Rameau Orlande de Lassus 10 most over-valued composers Johannes Brahms Camille Saint-Saens Charles Gounod Giuseppe Verdi Edvard Grieg Antonio Vivaldi Antonin Dvorak Pyotr Tchaikovsky Georges Bizet Giacomo Puccini Despite the presence of hype, though, the Amazon score and HA score agree pretty well with each other, as you see here:  The Spearman rank correlation between the two scores is +0.53 (p less than 10^-6). So, to some degree, the greater the esteem from encyclopedists, the more works are offered for sale. Still, differences in HA scores only account for under 30% of the variation in Amazon popularity, leaving plenty of room for the influence of hype. And do the P/E scores form a bell-shaped normal distribution? No. The average is 0.73 -- about what Domenico Scarlatti scores -- but most of the data are below this, and less above it. The graph below shows this skewed distribution, where most composers are actually rather under-valued and a handful are fairly over-hyped.  I don't have Amazon scores going back years -- or even one year -- so I can't make a series similar to the one that shows rising P/E ratios as the stock market enters a bubble, and declining values when the bubble bursts. I could find how many articles JSTOR contains that mention the composer, and measure this for all 69 composers across the years, and re-scale them by dividing by the maximum score in each year. But I'm not that interested in this topic, so I've done something a little different to detect bubbles. Murray also includes the year that each composer flourished -- i.e., when he turned 40 -- and I've plotted each composer's P/E score for the year he flourished. This allows us to see if composers from one time period are more or less over-hyped compared to those of another:  The composers of the pre-Classical periods (Medieval, Renaissance, and Baroque) are below-average in hype. Classical composers are average or a bit below, and the early Romantics are also about average. However, the late Romantics are vastly over-hyped. The Moderns are all over the place, although none is very over-hyped. It could be, though, that for the Moderns, an "overlooked" composer could have an unjustifiably high HA score, if Murray's article writers were not yet distanced enough to avoid the effects of recent manias for Modern composers. As a non-music buff, I feel my pedestrian tastes have been vindicated, as I've never gotten into the late Romantic period, but have always loved the Baroque most, then Classical, and even some early Romantic stuff. I have some catching up to do with Medieval and Renaissance composers, though. Culture mavens tell me that Baroque music is considered too nerdy and mostly suited for guy consumption, while the Romantics appeal more to normal people and women. So, music that appeals to more emotional people is over-valued, while music that appeals to more cerebral people is under-valued. This confirms that over-hyping something and an irrational, emotional mindset go hand-in-hand. On the topic of bubbles, Murray mentions that you do see fashion cycles, or booms and busts, in the percentage of an orchestra's output that comes from a particular composer -- e.g., that Bach might be very popular one year and decline for the next, say, 10 years. This is despite the fact that the aesthetic value of his work -- however we measure it -- hasn't changed. I think this argues against the cultural version of the efficient-market hypothesis. The public valuation of a composer may capture plenty of information about his fundamental worth, but there's a lot that's left out, such as the strong chance that a composer with a high P/E ratio owes some of his popularity to a bubble mindset among consumers. There are plenty of other cases you can apply this approach to, not to mention further refinements in looking at composers. What I'd really like to see is an objective measure of female celebrities' attractiveness -- say, by plugging measurements of their face, body, etc., into a regression equation -- and compare this against the number of results returned in a Google Image search for their name. I predict Angelina Jolie would score in the far-over-hyped range, Monica Bellucci in the average range of hype, and Jean Shrimpton in the over-looked range. Labels: arts, culture, Economics |

Razib's Home Page GNXP Archives Interviews Blogroll Principles of Population Genetics Genetics of Populations Molecular Evolution Quantitative Genetics Evolutionary Quantitative Genetics Evolutionary Genetics Evolution Molecular Markers, Natural History, and Evolution The Genetics of Human Populations Genetics and Analysis of Quantitative Traits Epistasis and Evolutionary Process Evolutionary Human Genetics Biometry Mathematical Models in Biology Speciation Evolutionary Genetics: Case Studies and Concepts Narrow Roads of Gene Land 1 Narrow Roads of Gene Land 2 Narrow Roads of Gene Land 3 Statistical Methods in Molecular Evolution The History and Geography of Human Genes Population Genetics and Microevolutionary Theory Population Genetics, Molecular Evolution, and the Neutral Theory Genetical Theory of Natural Selection Evolution and the Genetics of Populations Genetics and Origins of Species Tempo and Mode in Evolution Causes of Evolution Evolution The Great Human Diasporas Bones, Stones and Molecules Natural Selection and Social Theory Journey of Man Mapping Human History The Seven Daughters of Eve Evolution for Everyone Why Sex Matters Mother Nature Grooming, Gossip, and the Evolution of Language Genome R.A. Fisher, the Life of a Scientist Sewall Wright and Evolutionary Biology Origins of Theoretical Population Genetics A Reason for Everything The Ancestor's Tale Dragon Bone Hill Endless Forms Most Beautiful The Selfish Gene Adaptation and Natural Selection Nature via Nurture The Symbolic Species The Imitation Factor The Red Queen Out of Thin Air Mutants Evolutionary Dynamics The Origin of Species The Descent of Man Age of Abundance The Darwin Wars The Evolutionists The Creationists Of Moths and Men The Language Instinct How We Decide Predictably Irrational The Black Swan Fooled By Randomness Descartes' Baby Religion Explained In Gods We Trust Darwin's Cathedral A Theory of Religion The Meme Machine Synaptic Self The Mating Mind A Separate Creation The Number Sense The 10,000 Year Explosion The Math Gene Explaining Culture Origin and Evolution of Cultures Dawn of Human Culture The Origins of Virtue Prehistory of the Mind The Nurture Assumption The Moral Animal Born That Way No Two Alike Sociobiology Survival of the Prettiest The Blank Slate The g Factor The Origin Of The Mind Unto Others Defenders of the Truth The Cultural Origins of Human Cognition Before the Dawn Behavioral Genetics in the Postgenomic Era The Essential Difference Geography of Thought The Classical World The Fall of the Roman Empire The Fall of Rome History of Rome How Rome Fell The Making of a Christian Aristoracy The Rise of Western Christendom Keepers of the Keys of Heaven A History of the Byzantine State and Society Europe After Rome The Germanization of Early Medieval Christianity The Barbarian Conversion A History of Christianity God's War Infidels Fourth Crusade and the Sack of Constantinople The Sacred Chain Divided by the Faith Europe The Reformation Pursuit of Glory Albion's Seed 1848 Postwar From Plato to Nato China: A New History China in World History Genghis Khan and the Making of the Modern World Children of the Revolution When Baghdad Ruled the Muslim World The Great Arab Conquests After Tamerlane A History of Iran The Horse, the Wheel, and Language A World History Guns, Germs, and Steel The Human Web Plagues and Peoples 1491 A Concise Economic History of the World Power and Plenty A Splendid Exchange Contours of the World Economy 1-2030 AD Knowledge and the Wealth of Nations A Farewell to Alms The Ascent of Money The Great Divergence Clash of Extremes War and Peace and War Historical Dynamics The Age of Lincoln The Great Upheaval What Hath God Wrought Freedom Just Around the Corner Throes of Democracy Grand New Party A Beautiful Math When Genius Failed Catholicism and Freedom American Judaism

Archives

July 2005 August 2005 September 2005 October 2005 November 2005 December 2005 January 2006 February 2006 March 2006 April 2006 May 2006 June 2006 July 2006 August 2006 September 2006 October 2006 November 2006 December 2006 January 2007 February 2007 March 2007 April 2007 May 2007 June 2007 July 2007 August 2007 September 2007 October 2007 November 2007 December 2007 January 2008 February 2008 March 2008 April 2008 May 2008 June 2008 July 2008 August 2008 September 2008 October 2008 November 2008 December 2008 January 2009 February 2009 March 2009 April 2009 May 2009 June 2009 July 2009 August 2009 September 2009 October 2009 November 2009 December 2009 January 2010 February 2010 Hello Movable Type archives August 11,2002 August 18,2002 August 25,2002 September 01,2002 September 15,2002 October 20,2002 December 08,2002 December 22,2002 December 29,2002 January 05,2003 January 12,2003 January 19,2003 January 26,2003 February 02,2003 February 09,2003 February 16,2003 February 23,2003 March 02,2003 March 09,2003 March 16,2003 March 23,2003 March 30,2003 April 06,2003 April 13,2003 April 20,2003 April 27,2003 May 04,2003 May 11,2003 May 18,2003 May 25,2003 June 01,2003 June 08,2003 June 15,2003 June 22,2003 June 29,2003 July 06,2003 July 13,2003 July 20,2003 July 27,2003 August 03,2003 August 10,2003 August 17,2003 August 24,2003 August 31,2003 September 07,2003 September 14,2003 September 21,2003 September 28,2003 October 05,2003 October 12,2003 October 19,2003 October 26,2003 November 02,2003 November 09,2003 November 16,2003 November 23,2003 November 30,2003 December 07,2003 December 14,2003 December 21,2003 December 28,2003 January 04,2004 January 11,2004 January 18,2004 January 25,2004 February 01,2004 February 08,2004 February 15,2004 February 22,2004 February 29,2004 March 07,2004 March 14,2004 March 21,2004 March 28,2004 April 04,2004 April 11,2004 April 18,2004 April 25,2004 May 02,2004 May 09,2004 May 16,2004 May 23,2004 May 30,2004 June 06,2004 June 13,2004 June 20,2004 June 27,2004 July 04,2004 July 11,2004 July 18,2004 July 25,2004 August 01,2004 August 08,2004 August 15,2004 August 22,2004 August 29,2004 September 05,2004 September 12,2004 September 19,2004 September 26,2004 October 03,2004 October 10,2004 October 17,2004 October 24,2004 October 31,2004 November 07,2004 November 14,2004 November 21,2004 November 28,2004 December 05,2004 December 12,2004 December 19,2004 December 26,2004 January 02,2005 January 09,2005 January 16,2005 January 23,2005 January 30,2005 February 06,2005 February 13,2005 February 20,2005 February 27,2005 March 06,2005 March 13,2005 March 20,2005 March 27,2005 April 03,2005 April 10,2005 April 17,2005 April 24,2005 May 01,2005 May 08,2005 May 15,2005 May 22,2005 May 29,2005 June 05,2005 June 12,2005 June 19,2005 June 26,2005 July 03,2005 July 17,2005 August 07,2005 Blogspot archives June 2002 July 2002 August 2002 September 2002 October 2002 November 2002 December 2002

10 questions for....

Parag Khanna James Flynn Jon Entine Gregory Clark György Buzsáki Heather Mac Donald Bruce Lahn A.W.F. Edwards Luigi Luca Cavalli-Sforza Joseph LeDoux Matthew Stewart Charles Murray James F. Crow Adam K. Webb Justin L. Barrett David Haig Judith Rich Harris Ken Miller Dan Sperber Warren Treadgold Armand M. Leroi John Derbyshire

Blogs

The GiveWell Blog Your Religion Is False Colby Cosh Steve Hsu Audacious Epigone Catallaxy Files Inductivist 2 Blowhards Genetic Future Agnostic Steve Sailer Dienekes Derek Lowe Razib Khan Razib at Comment is Free Secular Right Glenn Reynolds Jim Miller Kevin McGrew John Hawks Peter Fost Randall Parker Less Wrong Charles Murray Carl Zimmer EconLog Marginal Revolution

Principles of Population Genetics

Genetics of Populations Molecular Evolution Quantitative Genetics Evolutionary Quantitative Genetics Evolutionary Genetics Evolution Molecular Markers, Natural History, and Evolution The Genetics of Human Populations Genetics and Analysis of Quantitative Traits Epistasis and Evolutionary Process Evolutionary Human Genetics Biometry Mathematical Models in Biology Speciation Evolutionary Genetics: Case Studies and Concepts Narrow Roads of Gene Land 1 Narrow Roads of Gene Land 2 Narrow Roads of Gene Land 3 Statistical Methods in Molecular Evolution The History and Geography of Human Genes Population Genetics and Microevolutionary Theory Population Genetics, Molecular Evolution, and the Neutral Theory Genetical Theory of Natural Selection Evolution and the Genetics of Populations Genetics and Origins of Species Tempo and Mode in Evolution Causes of Evolution Evolution The Great Human Diasporas Bones, Stones and Molecules Natural Selection and Social Theory Journey of Man Mapping Human History The Seven Daughters of Eve Evolution for Everyone Why Sex Matters Mother Nature Grooming, Gossip, and the Evolution of Language Genome R.A. Fisher, the Life of a Scientist Sewall Wright and Evolutionary Biology Origins of Theoretical Population Genetics A Reason for Everything The Ancestor's Tale Dragon Bone Hill Endless Forms Most Beautiful The Selfish Gene Adaptation and Natural Selection Nature via Nurture The Symbolic Species The Imitation Factor The Red Queen Out of Thin Air Mutants Evolutionary Dynamics The Origin of Species The Descent of Man Age of Abundance The Darwin Wars The Evolutionists The Creationists Of Moths and Men The Language Instinct How We Decide Predictably Irrational The Black Swan Fooled By Randomness Descartes' Baby Religion Explained In Gods We Trust Darwin's Cathedral A Theory of Religion The Meme Machine Synaptic Self The Mating Mind A Separate Creation The Number Sense The 10,000 Year Explosion The Math Gene Explaining Culture Origin and Evolution of Cultures Dawn of Human Culture The Origins of Virtue Prehistory of the Mind The Nurture Assumption The Moral Animal Born That Way No Two Alike Sociobiology Survival of the Prettiest The Blank Slate The g Factor The Origin Of The Mind Unto Others Defenders of the Truth The Cultural Origins of Human Cognition Before the Dawn Behavioral Genetics in the Postgenomic Era The Essential Difference Geography of Thought The Classical World The Fall of the Roman Empire The Fall of Rome History of Rome How Rome Fell The Making of a Christian Aristoracy The Rise of Western Christendom Keepers of the Keys of Heaven A History of the Byzantine State and Society Europe After Rome The Germanization of Early Medieval Christianity The Barbarian Conversion A History of Christianity God's War Infidels Fourth Crusade and the Sack of Constantinople The Sacred Chain Divided by the Faith Europe The Reformation Pursuit of Glory Albion's Seed 1848 Postwar From Plato to Nato China: A New History China in World History Genghis Khan and the Making of the Modern World Children of the Revolution When Baghdad Ruled the Muslim World The Great Arab Conquests After Tamerlane A History of Iran The Horse, the Wheel, and Language A World History Guns, Germs, and Steel The Human Web Plagues and Peoples 1491 A Concise Economic History of the World Power and Plenty A Splendid Exchange Contours of the World Economy 1-2030 AD Knowledge and the Wealth of Nations A Farewell to Alms The Ascent of Money The Great Divergence Clash of Extremes War and Peace and War Historical Dynamics The Age of Lincoln The Great Upheaval What Hath God Wrought Freedom Just Around the Corner Throes of Democracy Grand New Party A Beautiful Math When Genius Failed Catholicism and Freedom American Judaism   Policies Terms of use © http://www.gnxp.com Razib's total feed: |